8/8/22 The challenge of making ends meet… Inside July’s jobs report… A part-time-job boom (to pay the credit-card bill)… 500 million credit cards for the first time ever… Wall Street expects another 75-point hike… Good luck

Before we get into the featured article, let me share a quote, that I hope you will teach to your children, and never forget. “PROFITS are better than Wages” Jim Rohn

It literally is hard for me to understand how people living in America, the greatest free enterprise system the world has ever known, don’t really wrap themselves around this idea. Thankfully, I did an interview last week with a lady that gets it, You can see it here, and if you know someone like the Mr. Elliott talked about below, share it with them!

Originally Published by Stansberry Research

‘You have to pretty much rob Peter to pay Paul’…

Two months ago, with gas prices having hit all-time highs, Albert Elliott got a second job simply to afford to fill up his gas tank… so he could drive the 60 miles to his primary job at an Amazon warehouse in Raleigh, North Carolina…

He makes $15.75 per hour working for Amazon and, just to get to work, he took another job as a janitor at a community college, working an additional two days a week for $10 per hour. And that still wasn’t enough to make ends meet and fill up his Kia Soul completely…

As Elliott told the Washington Post last month, he paid for gas in increments of $15, $20, or $25 – whatever he could afford after spending his wages on essentials like food…

Unless it’s payday, I put in all the money I have at the time, sometimes borrowing money from family and friends… I began to realize that what I was making at Amazon was not enough to pay for gas. My biggest concern is not being able to get to work to make any money. You have to pretty much rob Peter to pay Paul.

I (Corey McLaughlin) don’t share this anecdote to simply depress anyone on a summer evening. Instead, especially since we’ve seen many similar anecdotes, it makes a critical point about the economy today – on the heels of a reported “strong” jobs report published late last week.

The disconnect couldn’t be clearer… and there will be consequences for the economy and markets.

The July jobs report blew past expectations…

The July jobs report blew past expectations…

This was the big headline, at least.

On Friday, the U.S. Bureau of Labor Statistics published its latest “nonfarm payroll” jobs report, and employment rose by 528,000 in July, and the unemployment rate dropped to 3.5% from 3.6% the month prior…

The numbers beat Wall Street’s expectations by a lot, as our Stansberry NewsWire editor C. Scott Garliss reported on Friday. That cranked up the expectation on Wall Street that with the job market so strong, the Federal Reserve has plenty of room to “fight inflation.”

That means the Fed will keep raising interest rates higher and higher. The idea is that if the economy keeps adding jobs while there are also 10.7 million unfilled jobs already, it has enough cushion to endure tougher conditions that will result from higher interest rates.

Scott is right, of course, about how Wall Street is viewing this report and how the Fed is likely to respond to it. But looking closer at the latest jobs data, you can see a few different realities of what’s happening on Main Street.

None of them strike me, at least, as showing a “strong” economy…

Instead, the details are more in line with the truth folks like Albert Elliott are facing in North Carolina. They need to make more money to make ends meet…

Digging into the details of the ‘hot’ jobs report…

Here are the red flags we see under the headline…

1) Of the 500,000-plus jobs the U.S. economy added in July compared to June, 384,000 were for part-time work… and 92,000 people added a second job, a trend that has accelerated since March. Meanwhile, in the past month, the economy lost 71,000 full-time jobs.

2) While the unemployment rate dropped slightly from June to July, so did the labor force participation rate. This means fewer people are working overall than a month earlier.

3) The biggest month-over-month gains were in part-time work and specifically in the services industry, like restaurants. And while the number of people working jobs lasting between one and three months increased, jobs of all other durations declined.

4) Wages ticked up, but not enough to keep pace with inflation. The average hourly wage for private-sector workers rose to $32.27 in July – a 5.2% annual increase – but well below 9.1% headline inflation over the same span.

This all jibes with recent data we’ve been tracking…

With inflation still high and the Fed hiking rates to slow down the economy, the number of job openings in the U.S. has been declining. Many companies have paused new hires or have started to lay folks off because of higher costs and less growth.

In the meantime, although some hourly wages are going up, workers aren’t making nearly enough to keep pace with inflation. This is a terrible scenario for pretty much everyone…

And it’s a result of pouring fire-starter – massive money-printing and near-zero interest rates – on a sizzling economy for much of the past two years. That stoked inflation (even before the war in Ukraine), and the Fed’s now playing catch-up.

Now, as Scott wrote on Friday, we’ve reached the messy dealing-with-the-consequences part of the story. Inflation is high and people are still spending money, of course. As he wrote, that “doesn’t help to combat inflation or intense demand for goods.”

So while on the surface, the economy adding 500,000 jobs might sound great, the details are uglier… The supposed strong July jobs report is more of an indicator about what inflation and a slowing economy are doing to people.

And there’s more…

Credit cards are booming…

Another sign showed up in another government report on Friday, which didn’t get nearly the mainstream coverage of the jobs report… We’re talking about credit-card balances.

According to the Fed’s consumer-credit report for June, overall debt rose by $40 billion in the month. That’s the second-largest increase in history, and it beat expectations by about $15 billion.

So-called revolving credit, which covers credit-card balances, was the main driver.

This report comes after a separate one from the New York Fed last week that said credit card balances increased by $46 billion from April to June, a 13% jump… and an additional 233 million new credit accounts – including credit cards as well as other personal loans –were opened in the second quarter, the most since 2008.

(Yes, that would mean basically one new credit account, on average, for roughly every U.S. adult. In reality, that means many people were opening multiple new credit accounts in that three-month period.)

According to a report from credit agency TransUnion published on Thursday, the number of total credit cards in the U.S. now exceeds 500 million for the first time ever, with 18-to-25-year-olds and subprime borrowers opening the most new accounts.

Turns out, more and more people are following Uncle Sam’s lead and spending money they don’t have more than ever… because there’s no other choice.

How long can it last? Well, as long as there are jobs. After that…

Despite this reality, here’s what the Fed is considering…

Again, the jobs report demonstrates that people are taking on more part-time, short-term work… while steady, full-time jobs are on the decline. Even so, many folks in positions of power care most about the headline numbers – including those at the Fed who are bent on manipulating our economy.

These are the same folks who, long ago, made decisions that got us to this point. And now, they’re planning to sacrifice economic growth in an effort to fight inflation, which may or may not work. (As Dan Ferris wrote on Friday, the Fed also cares about made-up numbers, too, like its 2% inflation target.)

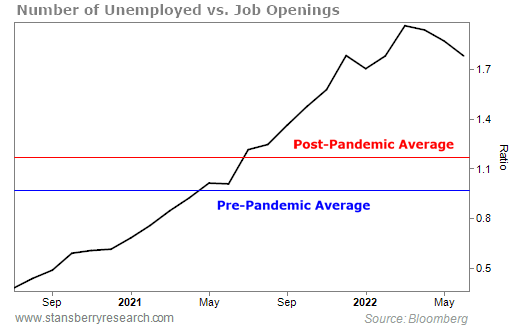

According to the latest jobs data, there are 1.7 job openings for every unemployed person. In theory, that means a lot of unemployed people could potentially get hired for two jobs today… and others who have one job have the ability to add another.

At least this is how the Fed sees it, as Scott wrote on Friday…

The Fed is trying to balance supply and demand in the labor market. It has said it wants to see the ratio between job openings and the number of unemployed people drop. The pre-pandemic average was around 1.0 compared with the current 1.2 and the March high of 2.0…

The trend in the jobs market is moving in the Fed’s preferred direction, Scott says, but it’s not nearly close to average levels… So that means more rate hikes (amid what is already an economic contraction, may we remind you)…

Wall Street traders are now betting on the Fed raising its benchmark lending rate by another 75 basis points at its next policy meeting in September, according to the CME Group’s FedWatch Tool.

That’s a reversal from what these same traders were expecting last week – before Friday’s jobs report. The odds were heavy on a 50-basis-point hike just one week ago… and one month ago. Such has been life in this inflation era.

At each of its policy meetings this year, the Fed has raised rates more than traders predicted. It hiked them not by 25 basis points, but 50. Not 50, but 75. These things were recently thought unimaginable to many folks, but now they’re accepted without much debate.

This is an undeniable trend that hasn’t broken yet as inflation has kept rising… So, all in all, know that the latest “strong” jobs report, counterintuitively, means the Fed has more reasons to sacrifice economic growth to fight inflation.

That means more pain for more people on Main Street, no matter how much they’re hurting already. Speaking of that, we still have this burning question to contend with…

Will inflation keep rising?

As we’ve said, “peak inflation” keeps going higher. Until this trend has clearly reversed, the Fed’s interest-rate hikes will be a concern. We’re still likely a long way from that point, but we’ll get more indications this week…

It’s another “inflation week,” meaning the government is set to publish its official consumer price index (“CPI”) and producer price index (“PPI”) monthly data, widely followed inflation gauges.

To set the stage, here’s the track of CPI – a gauge of prices everyday people pay for the same basket of goods each month – over the past few years…

On Wednesday, we’ll learn the CPI reading for July, and the next day we’ll get the PPI.

The PPI measures the wholesale prices producers pay for raw materials to make goods. Typically, this has been a leading indicator for inflation. And it has still been on the rise, including an 11.3% year-over-year gain in June – close to an all-time record.

As for answering the burning question…

If you’ve hoped for the best and prepared for the worst with inflation, as we’ve recommended since the beginning of the year, the answer today is to do more of the same.

Given the decrease in gas prices lately, the CPI could very well decrease from June’s measure, and we imagine that would be celebrated on Wall Street and elsewhere… But even if it does, that overshadows a bigger point.

Even if you hear “good news” on inflation this week, consider the context… Inflation is still near 40-year highs and isn’t likely to go back to any kind of pre-pandemic “normal” anytime soon, if not for many years. Meanwhile, the economy, as measured by gross domestic product, is still slowing.

Gas prices have come down over the past month or so, sure. That’s a welcome sign that inflation may be easing. But the damage to the economy from the great money-printing monetary experiment of 2020 and 2021 has been done… and it’s likely not over yet.

If the Fed sticks to its plan to fight the inflation it helped create, we’re likely to see more of a slowdown… more job openings disappear… more credit-card balances shoot to the moon… and more people take part-time jobs… and second jobs. In other words, we’ll see more Albert Elliotts.

Prepare accordingly. We’re not personal financial planners, but we’d encourage you to shore up your income streams as best as you possibly can. It’s also time to position and protect your investment portfolio for whatever comes next… the best, or the worst.